Imagine you've struck gold in the digital frontier. You've invested in cryptocurrency, and now you're seeing significant gains. But before you start counting your digital coins, have you considered the tax implications? The question on everyone's mind is: is crypto taxable? Understanding cryptocurrency taxation is crucial for anyone involved in the crypto space. Let's dive into the world of digital asset taxes and explore how to navigate the complex landscape of crypto tax strategies and reporting cryptocurrency gains.

Understanding Cryptocurrency Taxation

Cryptocurrency has revolutionized the way we think about money and investments. But with great power comes great responsibility—especially when it comes to taxes. So, is crypto taxable? The short answer is yes. Just like traditional investments, cryptocurrencies are subject to taxation. However, the rules can be a bit more nuanced.

The Basics of Crypto Taxation

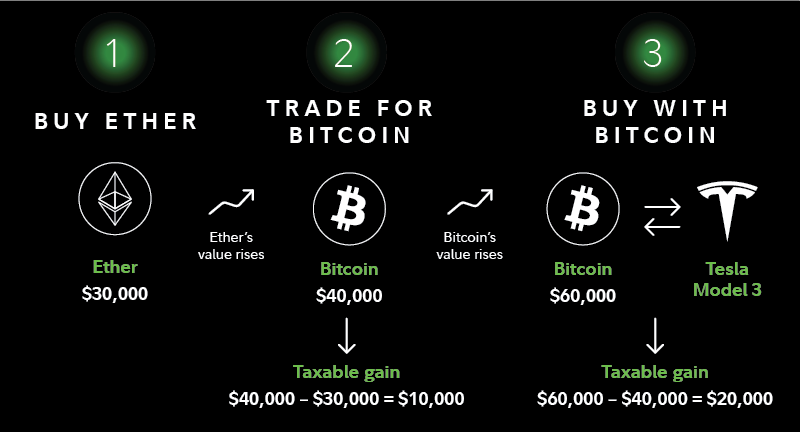

When you buy, sell, or trade cryptocurrencies, you're engaging in activities that can trigger taxable events. These events can include buying goods or services with crypto, trading one cryptocurrency for another, or converting crypto to fiat currency. Each of these actions can have tax implications of crypto that you need to be aware of.

For instance, if you buy Bitcoin and then sell it for a profit, you'll need to report that gain as capital gains. Similarly, if you use Bitcoin to buy a cup of coffee, the transaction is considered a sale, and you'll need to report the fair market value of the Bitcoin at the time of the purchase.

Types of Crypto Taxes

There are several types of taxes that can apply to your cryptocurrency activities. The most common are capital gains tax and income tax. Capital gains tax applies when you sell crypto for a profit. The amount of tax you pay depends on how long you held the asset—short-term gains (held for less than a year) are taxed at your ordinary income rate, while long-term gains (held for more than a year) are taxed at lower rates.

Income tax, on the other hand, applies when you receive cryptocurrency as payment for goods or services. This is considered ordinary income and is taxed at your regular income tax rate. For example, if you're a freelancer who accepts Bitcoin as payment, you'll need to report the fair market value of the Bitcoin at the time of receipt as income.

Navigating Crypto Tax Strategies

Now that you understand the basics of cryptocurrency taxation, let's explore some crypto tax strategies to help you minimize your tax liability. Just like in traditional investing, there are ways to optimize your crypto portfolio to reduce your tax burden.

Tax-Loss Harvesting

One effective strategy is tax-loss harvesting. This involves selling cryptocurrencies at a loss to offset gains from other investments. For example, if you have a significant gain from one crypto investment, you can sell another crypto at a loss to reduce your overall taxable income. This strategy can help you lower your tax bill while maintaining your investment portfolio.

Holding Periods

Another strategy is to hold your cryptocurrencies for more than a year. As mentioned earlier, long-term capital gains are taxed at lower rates than short-term gains. By holding your crypto for at least a year, you can take advantage of these lower tax rates and potentially save a significant amount on your taxes.

Tax-Free Exchanges

Some countries offer tax-free exchanges for certain types of cryptocurrencies. For example, in the United States, like-kind exchanges (also known as 1031 exchanges) allow you to swap one type of cryptocurrency for another without triggering a taxable event. However, this rule has been subject to change, so it's essential to stay updated on the latest regulations.

Reporting Cryptocurrency Gains

Accurate reporting is crucial when it comes to reporting cryptocurrency gains. Failure to report your crypto activities can result in penalties and interest charges. So, how do you go about reporting your gains?

Keeping Detailed Records

The first step is to keep detailed records of all your crypto transactions. This includes the date of the transaction, the type of cryptocurrency, the amount, the fair market value at the time of the transaction, and any fees paid. Keeping meticulous records will make it easier to calculate your gains and losses and ensure accurate reporting.

Using Crypto Tax Software

There are several crypto tax software tools available that can help you track your transactions and calculate your taxes. These tools can integrate with your crypto exchanges and wallets to provide a comprehensive overview of your crypto activities. Some popular options include [[CoinTracker]](https://www.cointracker.io/), [[TaxBit]](https://www.taxbit.com/), and [[CryptoTrader.Tax]](https://www.cryptotrader.tax/).

Consulting a Tax Professional

Given the complexity of cryptocurrency taxation, it's often a good idea to consult with a tax professional who specializes in crypto. They can provide personalized advice and ensure that you're compliant with all relevant tax laws. A tax professional can also help you identify potential deductions and credits that you may be eligible for.

Staying Informed and Compliant

The world of cryptocurrency is constantly evolving, and so are the tax regulations surrounding it. Staying informed about the latest changes in cryptocurrency taxation is essential for anyone involved in the crypto space. Regularly check for updates from tax authorities and consult with professionals to ensure you're always compliant.

Remember, the key to successful crypto investing is not just about making profits but also about managing your taxes effectively. By understanding the tax implications of crypto and implementing smart crypto tax strategies, you can maximize your gains and minimize your tax liability.

Conclusion

So, is crypto taxable? Absolutely. But with the right knowledge and strategies, you can navigate the complexities of cryptocurrency taxation and ensure that you're compliant with all relevant laws. Whether you're a seasoned crypto investor or just getting started, understanding your tax obligations is crucial. Keep detailed records, stay informed, and consider consulting with a tax professional to make the most of your crypto investments.

Now, it's your turn to take control of your crypto taxes. Start by reviewing your transactions, exploring tax strategies, and staying updated on the latest regulations. Your financial future depends on it.

FAQs

1. Do I need to report cryptocurrency transactions if I haven't sold any?

Yes, even if you haven't sold any cryptocurrency, you still need to report transactions such as buying goods or services with crypto, as these are considered taxable events.

2. What happens if I don't report my cryptocurrency gains?

Failure to report cryptocurrency gains can result in penalties, interest charges, and potential legal consequences. It's essential to accurately report all your crypto activities to avoid these issues.

3. Can I deduct crypto losses on my taxes?

Yes, you can deduct crypto losses to offset gains from other investments. This is known as tax-loss harvesting and can help reduce your overall tax liability.

4. Are there any tax-free ways to exchange cryptocurrencies?

In some countries, like-kind exchanges allow you to swap one type of cryptocurrency for another without triggering a taxable event. However, the rules can change, so it's important to stay updated.

5. How often should I review my crypto tax strategies?

It's a good practice to review your crypto tax strategies at least once a year, or whenever there are significant changes in tax regulations. Regular reviews can help you stay compliant and optimize your tax situation.

```

Posting Komentar